")

“The development of AI is as fundamental as the creation of the microprocessor, the personal computer, the Internet, and the mobile phone. It will change the way people work, learn, travel, get health care, and communicate with each other. Entire industries will reorient around it. Businesses will distinguish themselves by how well they use it.”

Bill Gates

“History is a story not only of the past, but of the future.”

Grace Lee Boggs

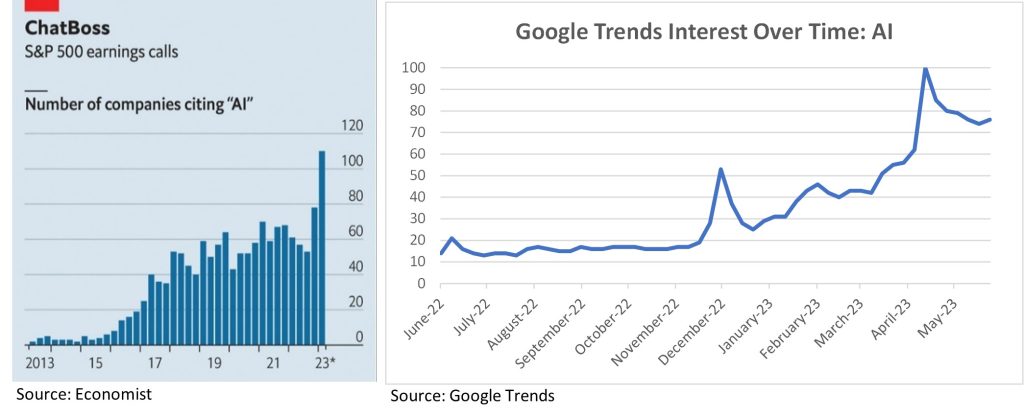

The rise of artificial intelligence (AI) has taken the world by storm. From healthcare and finance to transportation and entertainment, there seems to be no domain of human life immune from AI’s expanding reach. Curiosity surrounding this revolutionary technology is reflected in the surge of Google searches about the topic. The corporate world, too, has been caught up in this AI whirlwind, with nearly one in four S&P 500 companies referencing the technology during their most recent earnings call. As AI continues to advance at an astonishing pace, the allure of its transformative potential has propelled stocks of AI-related companies to new heights. An analysis by The Economist attributes nearly three quarters of this year’s stock market rally to 14 AI-related stocks. Since the start of the year, the price-to-earnings multiples of the S&P 500 excluding the AI-14 has kept steady at 27, whereas the average multiple of the AI-14 has increased from 43 to 77, indicating its rally is driven by heightened expectations rather than earnings growth. Has the hype outpaced reality?

Nvidia

Those seeking exposure to the AI gold rush are presented with a limited set of options. Being a new technology, AI has yet to produce pure-play public companies with a sole focus on the space. Those 14 stocks with the most AI exposure include big technology companies like Microsoft and Google. A significant portion of AI enterprises are in the venture stage and many future titans of AI are likely yet to be founded. As such, due to AI’s skyrocketing demand for computing power, the main beneficiaries of the recent craze have been the chipmakers. As the adage goes, the real fortunes of the 1800s gold rush were made by those selling picks and shovels, not digging for gold.

In the eye of this storm is Nvidia, the powerhouse behind the GPUs (Graphics Processing Units) that are the lifeblood of many AI systems. Its stock has soared, rallying 150% since the introduction of ChatGPT in November 2022. Nvidia finds itself in an enviable position, with over 80% market share in designing chips used by generative AI. The company’s edge extends beyond innovative chip designs. The demands of training AI models requires enormous processing power, often utilizing thousands of chips in tandem via a process known as advanced networking. Throughout the years, Nvidia invested heavily in this technology and now controls close to 80% of that market as well. Nvidia’s strength also lies in its software. Its AI platform, CUDA, enjoys popularity among programmers and is exclusively compatible with Nvidia’s chips. The company’s proactive engagement with the developer community predated similar attempts by competitors, further securing its edge in this growing market.

What’s not to like?

Sun Microsystems was one of the darlings of the dot-com era. The company is famous for creating many tools and systems in advancing several important areas of computing technology, including Java, a computer programing language. At its peak in 2000, Sun was worth $200 billion. In the subsequent year, its stock price dropped by 80% and was eventually sold to Oracle in 2010 for $7.4 billion, 96% below its peak. Here is what CEO Scott McNealy had to say to his investors after the dot-com crash:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

Nvidia’s stock currently trades at 40 times revenues. Even after accounting for analysts’ growth expectations, the stock trades at 10 times 2027 revenues. While Nvidia possesses a robust growth trajectory, much of that (if not more) is already baked into its valuation. We can’t ignore the potential risks and uncertainties that come with a still-nascent industry. The competitive landscape is a critical factor that could undermine these lofty aspirations. Established companies such as Intel and AMD are investing heavily in AI, while a myriad of start-ups are also hoping to carve out their niches. Both Amazon and Alphabet, through their respective cloud-computing divisions, are currently developing their own specialized AI chips. With their vast resources, these technology powerhouses may emerge as formidable rivals to Nvidia.

Governments also present a potential challenge for Nvidia. Regulators are increasingly concerned about the societal and national security implications of AI and are actively seeking methods to regulate the technology. There is an added geopolitical risk to consider in light of heightened military threats from China towards Taiwan. As Nvidia heavily relies on Taiwan for chip manufacturing, any potential disruption or geopolitical tensions could have adverse effects on the company’s supply chain and operations.

An Improbable Outcome

Nvidia’s ambitious stock price assumes its business will grow at an annual rate of 30% indefinitely. To gauge the plausibility of Nvidia’s success, a useful approach is to consider the historical performance of comparable companies. Just how persistent is the earnings growth of high-growth firms? A recent study by Verdad Capital shines a light on this very question with a sobering conclusion – only 3.6% of firms that achieved top-quartile earnings growth managed to maintain above-market growth rates five years down the line. Using history as our guide, Nvidia’s stock price is betting on a highly unlikely scenario.

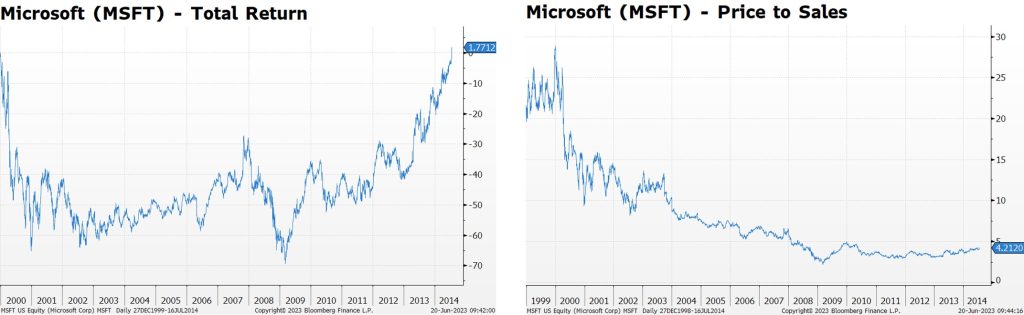

But what if, against all odds, Nvidia does sustain its superiority for another 25 years? In seeking a precedent for such sustained success, we find ourselves looking to Microsoft—a dot-com success story that not only maintained its grip on the PC market but also spread its influence across various tech realms, including the current sphere of artificial intelligence. At its peak in December 1999, Microsoft was trading at 28 times revenues, with a valuation just shy of $600 billion. In the subsequent decade, the tech giant grew its revenues every year and today stands as one of the most valuable companies in the world, boasting a market cap exceeding $2.5 trillion. However, those who dared to purchase its stock at the lofty 28 times revenues in December 1999 suffered a 65% loss on their investment in the subsequent year and had to wait 14 years to recoup their losses. This serves as a reminder of the long and uncertain road that buyers of Nvidia might have to tread.

Industry trend ≠ investment outcome

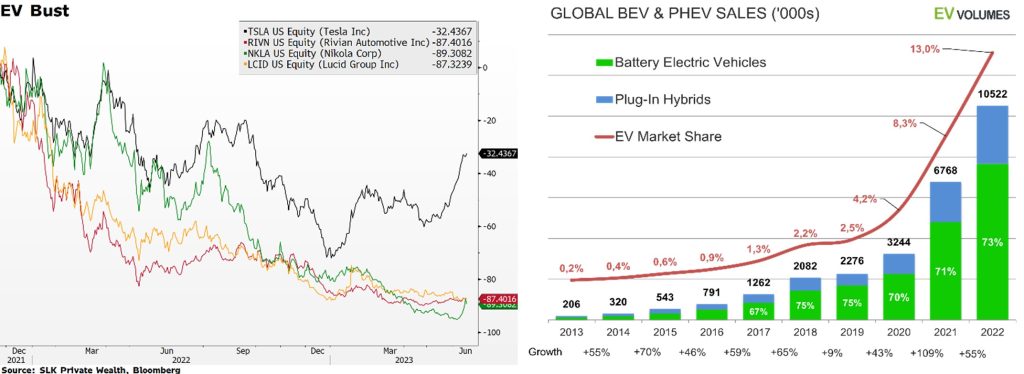

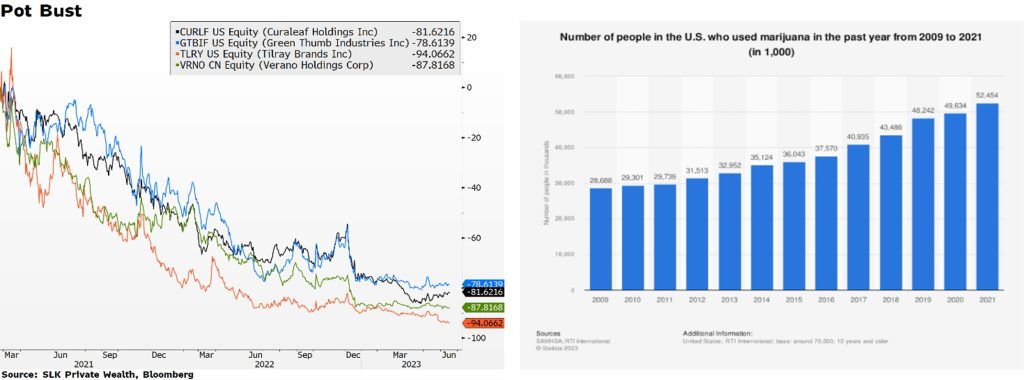

Investors tend to equate positive industry trends with promising investment returns. Yet history has time and again shown the fragility in this relationship. While the dot-com bubble serves as a classic example, let’s use more recent examples of such occurrences – electric vehicles and cannabis. Despite an acceleration in sales of electric vehicles, stocks of EV companies have plummeted by over 80% in the past 18 months. Investors, enthralled by the new technology, poured money into EV manufacturers even though many had yet to book a dollar in sales. The stocks of Rivian, Nikola and Lucid all peaked before delivering a single vehicle. Even Tesla, the trailblazer of the EV revolution, declined by 74% from its peak. As for cannabis, the true revolution was its legalization. Stocks like Tilray took hold of the public’s imagination and, for a time, commanded valuations exceeding $10 billion. Unfortunately, the high didn’t last, despite continued growth in consumption.

The sky-high valuations of Nvidia and other AI stocks point to the need for due diligence and restraint. As history vividly illustrates, transformative technologies can lead to speculative bubbles when hype outpaces reality. This is not to predict the bursting of an AI bubble or to denounce AI investments. Rather, it is to underscore the importance of sound investing principles. The excitement surrounding a company or an industry should never override the fundamental principles of valuation. While it’s true that revolutionary technologies can create enormous wealth, they can also precipitate devastating losses when bought at inflated prices. As ever, the price paid for an investment will play a pivotal role in determining its return. As the AI wave continues to gather momentum, it is essential to navigate this uncharted territory with prudence and discernment.

Razmig Der-Tavitian, CFA, CAIA

Chief Investment Officer

SLK Private Wealth